The Economics of Importing Gold from Dubai to India: Examining Price Differentials, Regulatory Frameworks, and Associated Risks

While gold prices are fundamentally determined in international markets denominated in US dollars, substantial differences in taxation, import duties, currency exchange rates, and local costs create persistent price discrepancies between Dubai and India that make cross-border gold purchases economically viable for many Indian buyers despite the associated regulatory and logistical complexities. This comprehensive analysis examines the structural factors that underpin these price differences, evaluates the actual financial advantages after accounting for all costs, and critically assesses both short-term and long-term risks inherent in importing physical gold from Dubai to India, revealing a nuanced economic picture that challenges the assumption of uniform international pricing.

The International Gold Market Structure and Price Determination Mechanisms

Global Pricing Framework and Local Variations

Gold is indeed globally priced in US dollars per troy ounce, with major trading happening on exchanges such as the London Bullion Market Association (LBMA), the COMEX in New York, and the Shanghai Gold Exchange. The London fixing serves as a crucial international benchmark that influences prices worldwide. However, while these international benchmarks establish a baseline, the retail price a consumer pays in any given country diverges significantly from this global spot price due to a complex interplay of local factors.

When gold prices are quoted internationally in US dollars, they must be converted into local currencies for domestic consumption. For India, this conversion happens at the prevailing USD-INR exchange rate, which fluctuates daily based on macroeconomic conditions, interest rate differentials, geopolitical developments, and capital flows. Since India is one of the world’s largest consumers of gold but produces virtually none domestically-manufacturing only about 1,000 kilograms annually while consuming approximately 800,000 kilograms—nearly all gold sold in India must be imported, making the exchange rate directly relevant to domestic pricing[2]. The formula that governs Indian domestic gold prices is straightforward yet consequential: the international USD price multiplied by the USD-INR exchange rate, with adjustments for import duties, taxes, and local margins.

Dubai, by contrast, operates within the UAE’s monetary system where the dirham (AED) is pegged to the US dollar at a fixed rate of approximately 3.67 AED per USD, creating a direct pass-through of international price movements without currency volatility. This structural difference alone means that currency fluctuations that might increase gold prices in rupee terms do not similarly affect the dirham price. Moreover, Dubai functions as a major global gold trading hub with significant volumes of physical gold inventory, allowing for highly competitive pricing that often tracks international spot prices very closely[7][10].

The Role of Supply, Demand, and Market Infrastructure

Beyond currency considerations, the sheer volume of gold trading and inventory positions in different markets creates pricing variations. Dubai’s gold market benefits from being a major re-export hub connected to global supply chains, with no value-added tax on bullion and investment-grade gold bars, and strict regulatory oversight by the Dubai Central Laboratories ensuring high quality standards[7][10]. This combination of regulatory certainty, tax advantages, and trading infrastructure creates an environment where gold can be sourced at very competitive prices relative to other global markets.

India’s gold market, while equally important in terms of demand volume, operates in an environment of higher taxation and import restrictions that push prices upward relative to the international baseline[1]. The Reserve Bank of India’s policies regarding gold imports, periodic adjustments to import duties by the government, and the implementation of goods and services taxes all create a domestic price premium. Additionally, Indian jewelers operate with cultural traditions that may include specific purity preferences and making charges that do not exist in Dubai’s more investment-focused market.

The Tax and Regulatory Architecture Driving Price Differences

India’s Current Tax Structure on Gold

As of 2026, India’s taxation framework on gold has undergone significant simplification following recent budget adjustments, yet substantial duties and taxes remain[1]. The basic customs duty on gold imports currently stands at approximately 5 percent, with an additional agriculture infrastructure and development cess of 1 percent, for a combined import duty of roughly 6 percent[3]. On top of this, a goods and services tax of 3 percent applies to the gold value itself[8]. For gold jewelry specifically, an additional 5 percent GST is levied on the making charges, which themselves range from 6 to 15 percent of the gold value depending on design complexity and brand reputation[8].

This represents a meaningful change from earlier years when import duties were substantially higher. According to an executive director at Motilal Oswal, before recent policy changes the total tax burden on gold purchases in India included import duties of approximately 12 to 13 percent, a cess of 1.5 percent, and GST of 3 percent, totaling roughly 15.5 percent in taxes alone[1]. The reduction of import duty from 12 percent to 2 percent (further refined to 5 percent basic customs duty) has substantially narrowed the tax-driven price gap between India and Dubai[1].

Dubai’s Value Added Tax and Exemptions

Dubai imposes a 5 percent value-added tax on gold jewelry but crucially exempts bullion and investment-grade gold bars (those with 99 percent or higher purity) from VAT entirely[7]. For tourists purchasing jewelry, the VAT is technically refundable upon export, though the process involves procedural complexity. This creates a situation where an investor purchasing investment-grade gold bars in Dubai faces zero VAT, while a jewelry buyer pays 5 percent VAT but may recover it. In contrast, an Indian buyer purchasing jewelry faces a 3 percent GST on the gold value plus 5 percent GST on making charges, generating a combined tax burden that exceeds Dubai’s structure for jewelry purchases.

Comparative Tax Calculations

To illustrate the magnitude of tax differences, consider a purchase of 100 grams of 22-karat gold.

In India, assuming a spot gold price of ₹14,300 per gram and a 10 percent making charge, the calculation would be: gold value of ₹14,30,000 plus making charges of ₹1,43,000, with 3 percent GST on gold value and 5% GST on making charges, totaling ₹50,050, yielding a final cost of approximately ₹16,23,050.

Summary Table of Corrected Prices for 100g 22K Gold in India

| Component | Amount (₹) |

|---|---|

| Gold Value (100g × ₹14,300) | 14,30,000 |

| Making Charges (10%) | 1,43,000 |

| GST on Gold Value (3%) | 42,900 |

| GST on Making Charges (5%) | 7,150 |

| Total Cost | 16,23,050 |

In Dubai, the same 100 grams at approximately 557 AED per gram (which converts to roughly ₹13,747 at the current exchange rate of approximately 24.67 AED per INR) would cost 55,700 AED in gold plus roughly 5 percent VAT of 2,785 AED if jewelry, totaling 58,485 AED or approximately ₹14,42,000 at current exchange rates. However, making charges in Dubai are typically lower, ranging from 5 to 10 percent, substantially reducing the final cost compared to India’s higher making charges.

Recent Price Comparisons and the Actual Savings Window

February 2026 Price Data

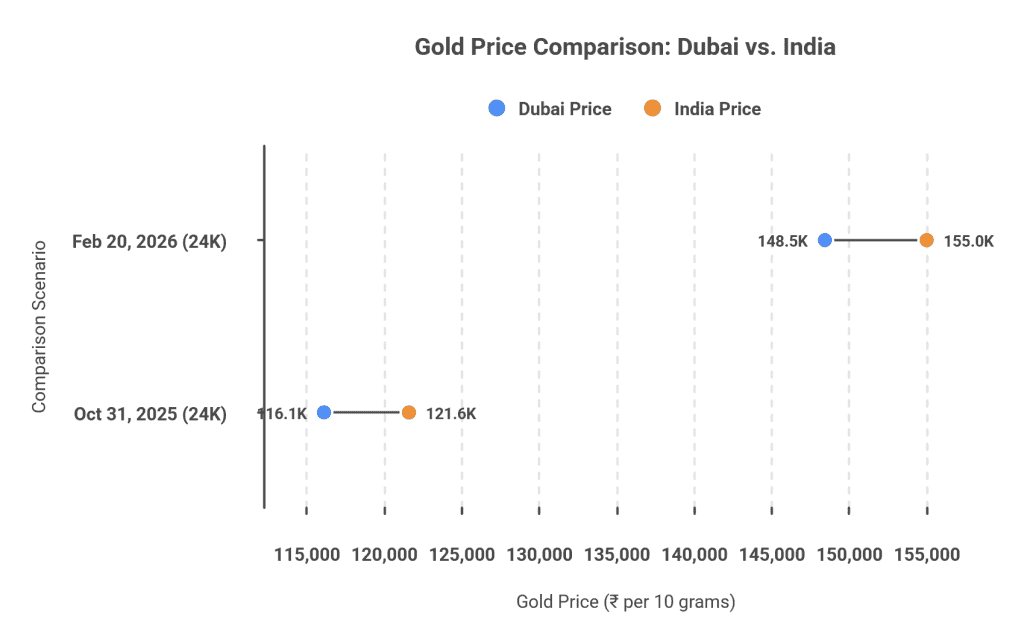

As of February 20, 2026, gold in Dubai was priced significantly lower than in India in absolute terms. Twenty-four-karat gold in Dubai cost approximately 601.75 AED per gram, converting to roughly ₹14,845 per gram or ₹1,48,451 per 10 grams at the prevailing AED-INR exchange rate. During the same period in India, 24-karat gold was trading at approximately ₹1,55,020 per 10 grams in New Delhi, ₹1,55,290 in Mumbai, and ₹1,55,080 in Kolkata, representing a price difference of approximately ₹7,159 per 10 grams in Dubai’s favor before accounting for any costs.

These raw price differentials represent the remaining gap after the Indian government’s reduction of import duties, suggesting that the approximately 5-7 percent raw price advantage Dubai maintains has narrowed considerably from the 15+ percent advantage that existed before duty reductions[1].

February 17, 2026 Comparison

On February 17, 2026, similar patterns emerged with 24-karat gold priced ₹6,650 lower per 10 grams in Dubai compared to India, and 22-karat gold priced approximately ₹4,711 lower. These fluctuations reflect the dynamic nature of international gold markets and exchange rate movements, indicating that the Dubai advantage fluctuates within a bandwidth typically between 4-7 percent on raw pricing.

October 2025 Comparison

Earlier in 2025, on October 31, the price differential was more pronounced, with Dubai offering 24-karat gold at ₹1,16,136 per 10 grams compared to India’s ₹1,21,620, a difference of approximately ₹5,484 or roughly 4.5 percent[4]. This pattern demonstrates consistency in Dubai’s pricing advantage despite global market volatility.

The Currency Exchange Rate Multiplier Effect

Rupee-Dollar Dynamics and Gold Pricing

The relationship between the rupee-dollar exchange rate and gold prices in India represents a critical but often overlooked factor in understanding import economics. When the Indian rupee weakens against the US dollar, imported gold becomes more expensive in rupee terms even if international dollar prices remain stable. Conversely, rupee appreciation makes imported gold cheaper locally without any change in global prices.

This currency effect operates independently of import duty changes and creates a dynamic pricing environment. A 2 percent depreciation in the rupee relative to the dollar could easily translate into a 2 percent increase in gold prices in rupee terms, potentially offsetting or amplifying the Dubai price advantage depending on the direction of movement. For an Indian buyer contemplating a Dubai purchase, favorable rupee movements could enhance the real savings, while adverse currency movements could diminish them.

The inflation expectations, interest rate differentials between India and the United States, and capital flow dynamics all influence the rupee’s trajectory, making it difficult to predict whether currency movements will favor or hinder gold imports from Dubai. Additionally, since Dubai’s AED is fixed to the US dollar, any depreciation in the rupee against the dollar automatically increases the rupee cost of Dubai gold without any corresponding increase in the dirham price—a mechanical advantage for Dubai that operates continuously.

The Complete Cost Analysis: Beyond the Raw Price

Visible and Hidden Transaction Costs

While the raw price differential appears modest at 4-7 percent after recent duty reductions, the complete economic analysis requires accounting for numerous additional costs that materialize during the import process. Travel expenses represent the first tangible cost, including airfare from India to Dubai and back, which can range from ₹15,000 to ₹40,000 depending on season, advance booking, and airline choice. For a buyer purchasing only 50-100 grams of gold—a relatively modest amount—these travel costs could consume a substantial portion of the raw price savings.

Customs duties on excess gold beyond the duty-free allowance represent another significant cost. Female Indian travelers can bring up to 40 grams of gold jewelry duty-free, while males are limited to 20 grams, provided they have stayed abroad for more than six months. Any gold beyond these limits faces a 6 percent customs duty if the traveler qualifies for concessional rates, or 36 percent for those not eligible[3][3]. This creates a substantial cliff effect where bringing slightly more than the allowed quantity triggers disproportionately high costs[3].

Making charges in Dubai, while generally lower than India’s 8-25 percent range, typically run between 5-10 percent of the gold value. If a buyer purchases jewelry in Dubai rather than bullion, these making charges, combined with the 5 percent VAT (though theoretically refundable for tourists), increase the effective cost significantly. For a tourist purchasing ₹100,000 of jewelry in Dubai at 8 percent making charges, the total would be ₹108,000 before VAT, and ₹113,400 after VAT, approaching or exceeding what an equivalent India-purchased item would cost when accounting for different making charge structures.

Insurance and Documentation Costs

Carrying gold across international borders necessitates insurance protection against loss or theft, a cost that varies between ₹500 and ₹2,000 depending on the value and coverage duration. Additionally, buyers should budget for proper invoices, purchase receipts, and potentially export certificates from Dubai customs, which require time and administrative effort. For those importing jewelry, obtaining purity certificates or having gold tested at a BIS-accredited center in India incurs costs of ₹200 to ₹500 per item.

Opportunity Costs and Time Factors

The opportunity cost of traveling to Dubai specifically for gold purchases—including time away from work or other activities—represents an implicit economic cost that varies dramatically by individual circumstances. A professional who forgoes ₹20,000 in work income to save ₹5,000 on gold has actually lost money from an economic perspective, though such calculations are highly subjective.

Short-Term Risks and Regulatory Complications

Customs Declaration and Duty Exposure

The immediate and most tangible risk for Indians bringing gold from Dubai involves customs compliance and duty payment at Indian airports. The regulations are explicit: any gold jewelry exceeding the duty-free allowance becomes liable to customs duty, and failure to declare triggers potential confiscation and penalties. Multiple recent cases demonstrate that customs enforcement has intensified, with officers employing advanced screening techniques including X-ray examination, metal detectors, and profiling to identify gold smuggling attempts.

A February 2026 incident at Delhi’s Indira Gandhi International Airport involved a passenger attempting to smuggle 170 grams of gold hidden inside a beverage bottle cap—a creative concealment that was nonetheless detected, resulting in seizure and ongoing investigation. Another case from the same period involved gold paste concealed in underwear and socks. These examples underscore that customs authorities employ increasingly sophisticated detection methods and that attempted evasion—even of relatively modest quantities—carries serious legal consequences including confiscation, fines, and potential prosecution.

The Mathematics of Customs Duty on Excess Quantities

For a female traveler bringing 50 grams of gold jewelry when the duty-free limit is 40 grams, the excess 10 grams would face a 6 percent concessional duty if imported through proper channels, amounting to approximately ₹600 on a ₹10,000 value (assuming ₹1,000 per gram). However, bringing 100 grams would make 60 grams subject to duty, and attempting to circumvent declaration would expose the entire 100 grams to 36 percent duty (₹3,600) if discovered by customs, plus potential fines and legal complications[3]. The risk-reward calculus shifts dramatically once quantities exceed the duty-free limits by meaningful amounts, making smuggling attempts economically irrational for small quantities despite the temptation[3].

Regulatory Changes and Policy Uncertainty

India’s gold import policy has experienced several significant changes in recent years, including the 2012-2013 80:20 import-export scheme that restricted domestic sales of imported gold, followed by subsequent revisions and eventually modifications to import duty rates[2]. The budget changes of 2024 that reduced import duty from 12 percent to 5 percent basic customs duty plus 1 percent cess represent major policy shifts that benefited importers but also demonstrated the government’s propensity to adjust gold trade policy[1].

Short-term policy uncertainty represents a genuine risk for those importing gold based on current duty rates, as demonstrated by the government’s history of tariff adjustments. If the government were to reverse course and increase import duties—responding to revenue pressures or fiscal consolidation requirements—individuals who brought gold in anticipating continued low duties could face regret and potential pressure to re-export at unfavorable prices.

Authenticity and Purity Verification Challenges

Another short-term risk involves verifying gold authenticity and purity when purchasing in Dubai without extensive testing infrastructure readily available. While Dubai maintains rigorous quality standards through its Central Laboratories, individual buyers may lack the expertise to distinguish between genuine 24-karat and 22-karat gold or to identify potential adulteration. Upon return to India, having gold tested at a Bureau of Indian Standards (BIS) accredited laboratory mitigates this risk but adds cost and time delays.

Some unscrupulous jewelers in Dubai have been known to misrepresent purity or quality to tourists who cannot immediately verify claims, a risk that is lower for established retailers but non-zero for exploratory shoppers. The legal recourse available if gold purchased in Dubai proves to be misrepresented is limited, as Indian consumer protection laws have limited extraterritorial reach.

Health and Safety Risks During Travel

Carrying substantial quantities of gold creates personal security risks, including exposure to theft or robbery during travel between Dubai and home, at airports, or during transportation. While the probability of such incidents is low, the concentrated value of gold means that losses—if they occur—can be substantial. Insurance mitigates but does not eliminate this risk, and claims processing can be time-consuming and contentious.

Medium-Term and Long-Term Risk Considerations

Currency Fluctuation and Reverse Price Movements

While short-term currency movements can enhance savings, extended periods of rupee appreciation against the dollar could create a situation where Indian domestic gold prices decline relative to Dubai prices, reversing the economic advantage. If an individual purchases gold in Dubai based on current favorable pricing but finds that over subsequent months the rupee strengthens by 5 percent, the real rupee value of that Dubai-purchased gold effectively decreases while domestically purchased gold maintains relative stability—a form of currency risk that extends the import transaction beyond its immediate completion.

The unpredictability of multi-month currency movements means that individuals banking on persistent Dubai price advantages face genuine macro-level uncertainty. A rupee appreciation from 100 INR per USD to 95 INR per USD would simultaneously reduce Dubai gold prices in rupee terms by approximately 5 percent while making imports less economically attractive.

Gold Market Volatility and Price Risk Exposure

Gold prices globally experience volatility driven by interest rate expectations, inflation dynamics, geopolitical tensions, and safe-haven demand shifts. While this volatility affects both Dubai and Indian prices similarly, it introduces the risk that gold purchased in Dubai for ₹100 per gram could decline to ₹95 per gram within months, eroding the original purchase advantage. Conversely, prices could rise, benefiting the purchaser, but the fundamental point is that importing gold based on current price spreads exposes individuals to subsequent volatility risk.

This risk is partially mitigated if the purchaser views the gold as a long-term store of value rather than a trading commodity, but for those importing with the intent to sell domestically (perhaps to meet a wedding requirement or unexpected financial need), price volatility could eliminate the original savings advantage.

Tax Policy Evolution and Retrospective Complications

India’s evolving tax policy on gold creates long-term uncertainty. The government has demonstrated willingness to adjust duties, implement new tax categories, and introduce anti-smuggling measures. If retrospective or anti-evasion provisions were ever introduced—for example, creating disclosure requirements or establishing a “black gold” identification system—individuals who imported gold under earlier regulatory environments could face complications or additional taxation.

While retrospective taxation is generally disfavored in democratic systems with rule-of-law traditions, the precedent of implementing gold monetization schemes and reporting requirements demonstrates the government’s evolving approach to gold holdings. Any new scheme that requires proof of legal acquisition could theoretically create complications for gold purchased through informal cross-border channels, even if the purchase was itself legal.

Relationship to Formal Financial Systems and Capital Controls

Carrying gold across borders and importing it through personal travel rather than through official import channels represents a departure from formal financial system documentation. If India were to strengthen capital control frameworks or introduce financial asset reporting requirements, individuals with substantial undocumented gold holdings might face scrutiny. While this risk is low in the current regulatory environment, it exists in principle and could materialize if fiscal pressures drive comprehensive wealth assessment initiatives.

Opportunity Cost of Capital Deployment

From a long-term wealth creation perspective, capital deployed in gold imports could alternatively be invested in equity markets, fixed-income instruments, or other productive assets. Gold has historically provided returns that roughly match inflation but have underperformed equity markets over extended periods. An individual importing gold and holding it faces an implicit opportunity cost relative to other investment options, particularly if the Dubai purchase was undertaken primarily for perceived economic advantage rather than cultural or jewelry preferences.

Strategic Alternatives to Direct Physical Imports

Domestic Gold Schemes and Formal Channels

The Indian government offers several formal mechanisms for gold acquisition that avoid the regulatory and logistical complexities of cross-border imports:

Sovereign Gold Bonds (SGBs): These debt instruments issued by the Reserve Bank of India provide returns linked to gold prices while delivering interest income of 2.5 percent annually. SGBs offer tax advantages compared to physical gold and avoid import complexities entirely. For long-term wealth accumulation focused on gold exposure, SGBs represent an alternative mechanism that aligns with formal financial systems.

Gold Mutual Funds and ETFs: Exchange-traded funds tracking gold prices provide exposure to gold price movements without physical storage, purity verification, or import complications. These instruments trade on Indian stock exchanges and offer liquidity advantages compared to physical gold.

Domestic Gold Loans: Jewelers and banks offer gold loans against physical gold collateral, allowing individuals to finance purchases through formal credit channels while maintaining access to government and institutional pricing.

Bulk Import Through Licensed Dealers

Rather than personal travel-based imports, individuals can acquire Dubai-sourced gold through licensed gold importers and authorized dealers who operate formal import channels, handle all customs documentation, and provide proper invoicing. While this eliminates travel costs and personal customs risk, it typically reduces the raw price advantage to 2-3 percent due to dealer markups and formal compliance costs.

The Economics Summary: When Dubai Imports Make Financial Sense

Scenarios Favoring Dubai Purchases

Dubai gold imports generate net economic benefits in the following scenarios:

- Large Quantity Purchases: When an individual is purchasing 200+ grams of gold, the amortized travel costs, insurance, and customs duty become proportionally smaller relative to the raw price savings. At this quantity level, a 4-7 percent raw price advantage could translate into ₹15,000-30,000 in net savings even after accounting for all costs.

- Jewelry with Specific Designs: If an individual requires jewelry with specific designs, artistry, or quality standards available primarily in Dubai, the Dubai purchase becomes justified on non-price factors. The comparative price advantage becomes secondary to design quality.

- Favorable Currency Windows: During periods of significant rupee depreciation (₹105+ per USD), the relative advantage of Dubai purchases expands, making the time investment more economically rational.

- Multiple Family Members: When several family members travel together to Dubai, the per-capita travel costs decline dramatically. A family trip that brings 5-6 members can allocate gold purchase costs across all travelers, making the economics substantially more favorable.

- Tax-Advantaged Holdings: Non-resident Indians (NRIs) with different tax treatment may find Dubai purchases offer advantages unavailable to resident Indian citizens, particularly regarding offshore holdings and documentation.

Scenarios Where Domestic Purchasing Dominates

Conversely, domestic gold purchases become preferable when:

- Small Quantities: Purchasing fewer than 50 grams makes travel costs prohibitive relative to savings.

- Jewelry with Making Charges: If jewelry making is required, Dubai’s quality advantage does not overcome the time and hassle costs of international coordination.

- Immediate Need: Wedding dates and other time-sensitive requirements make domestic purchases more practical.

- Risk Aversion: Individuals uncomfortable with customs procedures, documentation, or regulatory uncertainty logically prefer the simplicity of domestic purchases.

- Rupee Appreciation Expectations: If macroeconomic forecasts suggest incoming rupee strength, delaying purchases until rupee appreciation materializes makes more economic sense than importing at current rates.

Conclusion: A Narrowing Arbitrage With Persistent Frictions

The gold price differential between Dubai and India has narrowed substantially following the 2024-2025 reduction in Indian import duties from 12 percent to 5 percent (plus 1 percent cess), reducing what was historically a 15+ percent tax-driven advantage to a current 4-7 percent range reflecting primarily currency effects, exchange rate pass-through differences, and market microstructure variations rather than fundamental policy distortions.

When accounting for travel costs, insurance, customs duty exposure on excess quantities, making charges, documentation, and time costs, the raw price advantage of 4-7 percent frequently becomes a modest net advantage of 1-3 percent for optimally-sized purchases. This remaining advantage is real but substantially smaller than commonly perceived, and depends sensitively on transaction size, currency movements, and individual opportunity costs.

Short-term risks include customs duty exposure for excess quantities, regulatory policy changes, authentication challenges, and personal security during transport. Long-term risks include currency fluctuation reversals, gold market volatility, evolving tax policy, and the opportunity cost of capital not deployed in higher-yielding assets. These risks are not catastrophic for compliant, reasonably-sized imports, but they are material enough to warrant careful analysis before undertaking Dubai purchases.

For individuals making large purchases (200+ grams), traveling with multiple family members, seeking specific jewelry designs, or possessing exceptionally favorable currency windows, Dubai imports can generate meaningful net economic benefits despite all costs and risks. For smaller purchases, immediate needs, or risk-averse individuals, the superior simplicity and certainty of domestic purchases likely outweigh the modest theoretical savings available through cross-border imports. The decision ultimately depends on individual circumstances, risk tolerance, and the specific characteristics of the gold being sought.

References:

- https://www.hindustantimes.com/trending/is-it-cheaper-to-buy-gold-in-dubai-rather-than-india-motilal-oswal-executive-answers-101760852771223.html

- https://finshots.in/archive/the-glittering-allure-why-gold-smugglers-like-india/

- https://mumbaicustomszone3.gov.in/import-guidelines-for-gold-valuable

- https://www.angelone.in/news/commodities/india-vs-dubai-gold-rate-understanding-the-price-difference-on-october-31-2025

- https://globalbullionsuppliers.com/en-us/blogs/blog/why-is-gold-smuggled-to-india

- https://www.newindianexpress.com/explainers/2026/Feb/21/us-supreme-court-ruling-on-tariffs-what-changes-and-what-doesnt-for-india

- https://sanajewellers.com/blogs/news/how-to-identify-authentic-gold-jewellery-in-dubai

- https://www.dreamticket.co.in/gold-jewellery-making-charges/

- https://www.goinri.com/blog/how-much-gold-can-i-carry-from-the-usa-to-india

- https://www.mygoldguide.in/understanding-rules-hallmark-gold-in-dubai

By

By